")

The earlier you start, the more money you can earn, the more time you have to carry out your plan & make changes to it. The better your strategy can withstand unforeseen circumstances. You’ll have the luxury of saving less per month to reach your goals later.

A. Why you should start your plan today.

A1. A longer time frame to plan, adjust & create redundancy.

Imagine having a goal(s), [applying for BTO ($30k) -> getting married at a wedding ($20k) -> renovation of BTO ($20k) -> 1st child ($10k)], in typical Singaporean fashion that will happen in that order & adding up the costs, you’ll have to fork out over $80 000 total ($40 000 split between each partner) in a possible short time span of a conservative 6 years. Where would you come up with such a large amount? Take a loan from your parents, friends or worse still; the banks? As much as possible, you can only cut & trim out so much from costs from the expenditures but you’ll still have to spend a substantial amount of money to at least have a decent experience.

By starting early (AKA now), you can easily squirrel away a smaller amount of money a month to reach these goals, cutting out the worry of not having enough, not having a good experience (plus FOMO of not getting those IG worthy moments) & ‘oh what will those pesky & annoying relatives / friends (that love to compare) say?’

Perhaps some unforeseen event happens (loss of income, substantial medical bills etc) that derails your plans for the near future, preparing now would give you more time to readjust, trim out non-essential plans. The fact of life is that we will never know what will happen to our lives or the lives close to us, BUT having more money (from your plans from years back) helps to creates redundancy that will definitely give you or your loved ones some peace of mind.

A2. More time to save = more money to spend

When we’re young, we think we are invisible; none of those stories we hear from peers would ever happen to us right? The young have time & the time will never come back once wasted away. Let’s take for example 2 characters, Mr A & Mr B having the same goal of trying to save $40 000 by 30 years old. Mr A who started saving at age 20 has 10 years to save $40 000 starting from $0 in his bank account, he would have to save ~ $333 a month to reach that goal. Whereas Mr B who only started saving at age 25, he would have to save ~ $666 which is 2 x more than Mr A. Which method do you think is easier & less stressful for an individual such as yourself? Obviously the method of Mr A, having started earlier, he can set aside a smaller amount per month leaving more each month for himself to spend on things he likes.

A3. More time to allow compound interest to work

We will be using compound interest a lot to build wealth. The quote ‘ The best time to plant a tree was 20 years ago, the next best time is now ‘ resounds really well with the use and eventual effects of compound interest. We are limited by our life spend here on earth, further exacerbated by our available working years till we get retrenched / retire. So start now.

A4. Creates the discipline & a system (a habit) to make monetary decisions faster and easier

The earlier we start building & reinforcing good habits, the easier it is to let these habits assimilate into our everyday lives till it can become a subconscious effort. Think of money as an enabler & a tool to our basics needs, wants & also for self improvement / self wellness courses (products etc)

A5. Time to recover from mistakes (inevitable, lack of foresight)

It would be inevitable for the best of us / the majority of us that we will make some form of mistakes or losses (investing mistakes, business venture losses, losses due to friends cheating your money). The extra time we have gleaned from starting early will help us recover & bounce back faster.

B. How compound interest can work in your favour.

B1. Compound Interest works best with time (a lot of time)

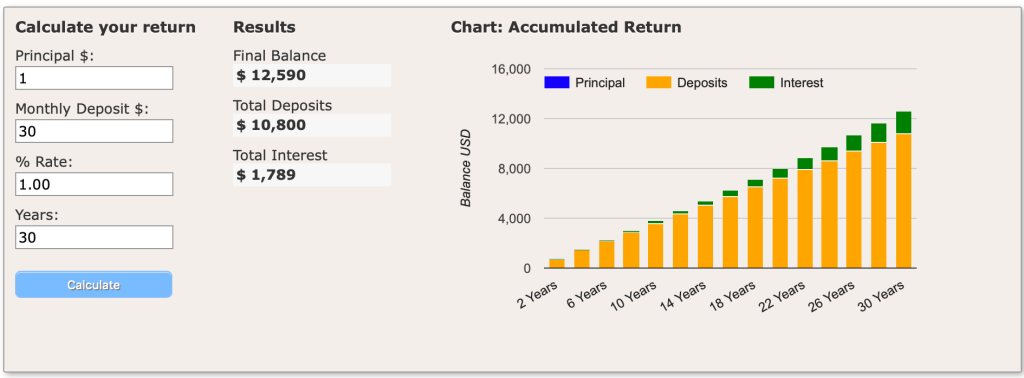

Here’s a graph to illustrate what compounding can do. 1% more every day, builds upon the previous days to further your returns (be it money, results or habits)

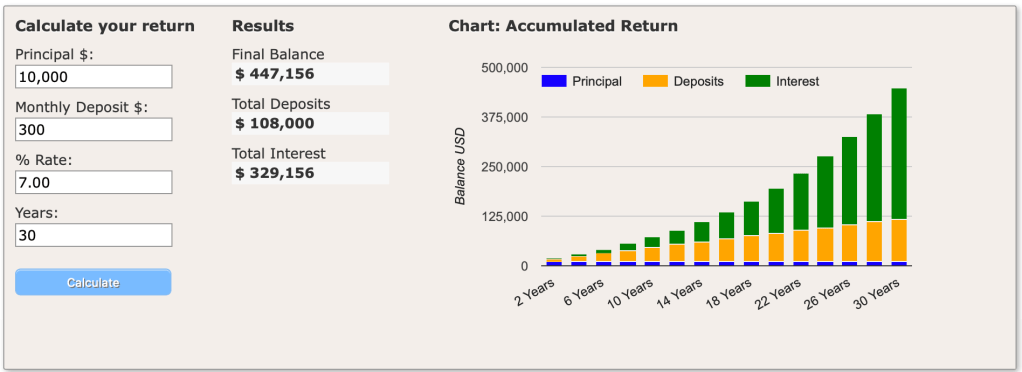

Now take into account investing money, if you started investing today with a principle of $10 000, plus adding a monthly contribution of $300 for 30 years. This is what you’ll get:

The effects are more pronounced as the growth is exponential. This is not factoring in market crashes & recessions yet though.

B2. Combat against inflation, lifestyle changes (medical, higher living standards), rise in cost of living, loss in purchasing power

We’ve talked about how normal inflation & lifestyle inflation affects our spending power. Normal inflation is natural & it is beyond our control. Lifestyle inflation is a choice for the most part but we cannot reduce it too much till we do not enjoy life. Whatever it is, these forces of nature / environment will eat into our spending power, which we all wish to beat.

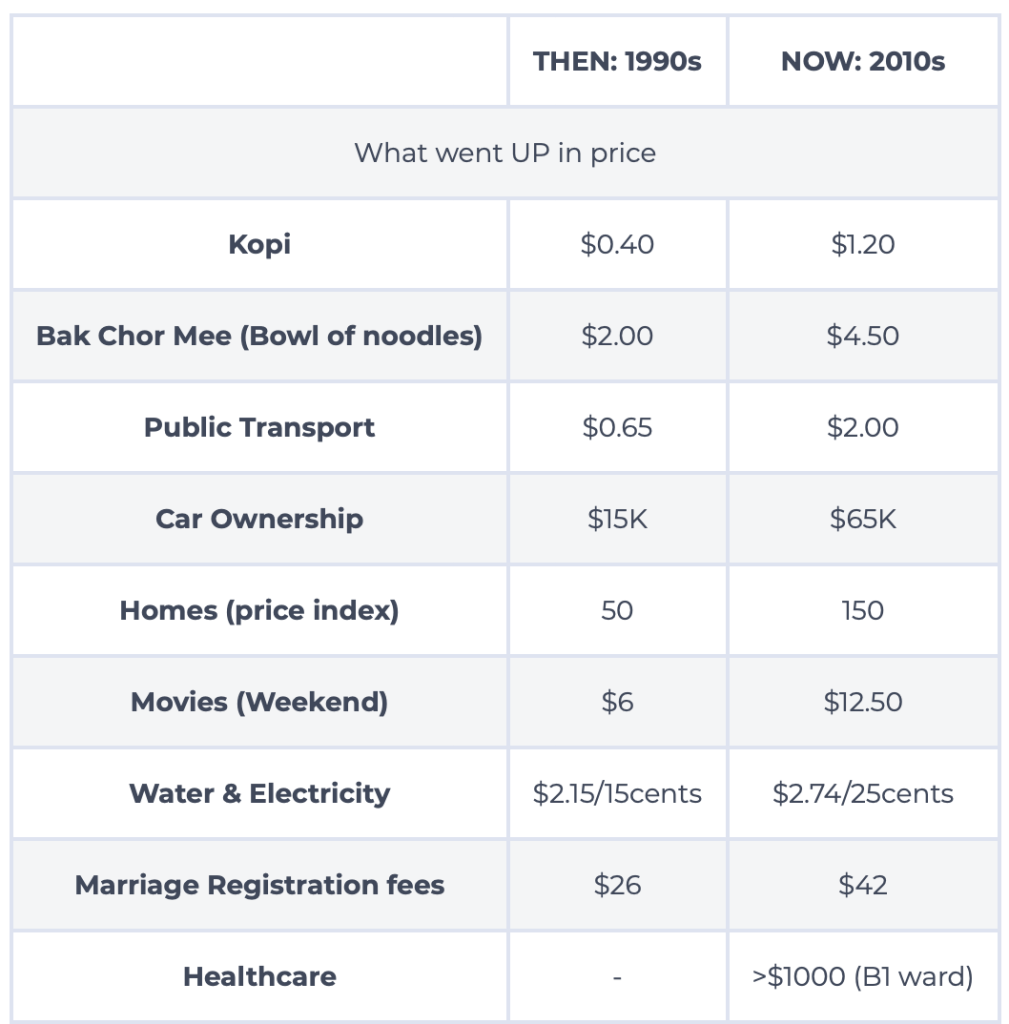

Here’s a comparison between basic necessities from the past & the present.

B3. Allow you to ironically have peace of mind (hedge against the loss of your primary source of income)

Money tends to be the core of problems, especially in relationships (more so in the Asian context?) Especially so when we are taught to save, save & save more for a rainy day, but we then end up having to spend a substantial amount of money on Housing, Living Expenses, Raising Children till Adulthood, Holidays & Medical Bills, all of which brings about added stress into our lives. Ironically, we’re encouraging people to invest on stocks in the Stock Market, stuff that is foreign, scary & potentially harmful if undertaken without proper knowledge. IF we overcome all that fear (aversion to losing money), understand & respect the power of investments, we can potentially come out financially better off, thus giving us some peace of mind.

B4. Increase the time value of money

The Time Value of Money states that rational people (investors) prefer receiving a similar sum of money now versus in the future (eg. 1 year later), simply due to the fact that inflation will eat away at the value of money. The value of money NOW will always be stronger than received at a later date (if no interest is worked on that amount). With compounding (at any rate higher than current inflation levels), the Time Value of Money in the future will definitely be worth more than the present; thus increasing your spending power.

C. How compound interest can work against you.

C1. Credit Card Debt – Compounds at a daily rate (or any form of debt with interest rates eg. student loans)

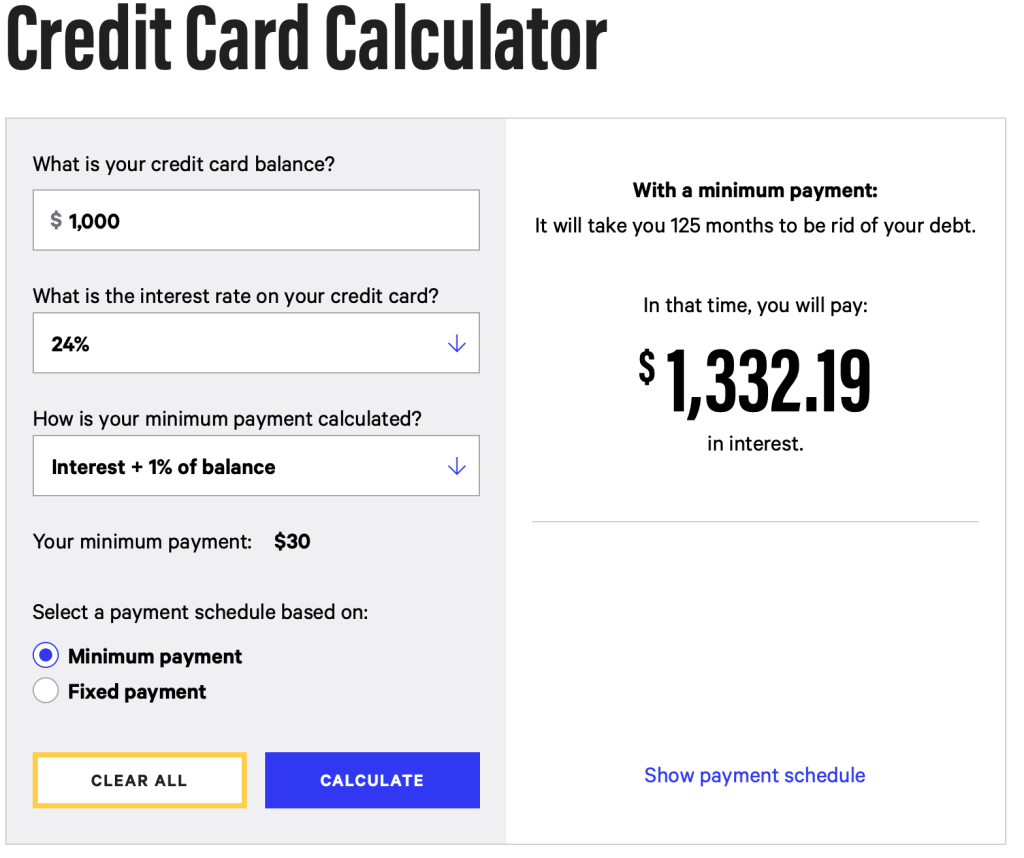

Most credit card debt compounds on a daily rate even at seemingly low interests rates (0.0000137%) – compound this every day (interest rates works on the previous day’s total in perpetuity till you pay off the debt). Enter Annual Percentage Rates (APR) which may amount to 24% / annum or 2% a month COMPOUNDED. Here’s a look at the possible fees you’re indebted to pay of you’re not using these cards wisely.

C2. CPF OA usage to pay back the housing loan

Truly a Singaporean problem, having to pay back the principle loan amount + the accrued interest on what your CPF OA could have earned had it not been withdrawn. As long as the HDB flat is not sold, you don’t have to pay the interest back (yet). Side tracking away, your CPF account wasn’t initially meant to pay for housing loans but rather a base layer of income for retirement.

C3. HDB Houses are a depreciating asset after a threshold age

Paying back the loan + accrued interest to your CPF OA would really reduce your monies required for retirement; thus setting you back financially for retirement (sales proceeds from your HDB flat will go back to CPF first).

D. Ways to utilise compound interest

D1. Investing

Investing monies that you’ve set aside into stocks through the local stock exchange (SGX) & / or foreign / international stock exchanges (NASDAQ, NYSE, LSE, HKSE). Armed with investing knowledge, money & guts to manage risk, the potential returns from investing outweighs the cons of not investing. Simply due to the fact that you’ll automatically lose out to inflation when you don’t do anything with your money.

D2. CPF Top Ups

Topping up your retirement fund (CPF SA) via Retirement Sum Top Up (RSTU) or Voluntary Contribution (VC) which can provide tax relief . Utilising the guaranteed interests rates on your CPF accounts can help you compound your savings to a substantial amount. Some gutsy folks dubbed their movement as 1M65 (achieve 1 Million Dollars in CPF Accounts by 65 years of age). Whatever it is, it is prudent to at least pump money into your CPF Special Account to (1) Reach Full Retirement Sum (FRS) ASAP, (2) Get Tax Relief with the Top Up. Again due to inflation, the FRS will increase every year as it has for the last 10+ years.

D3. Regulated Lending

Lending money to Start Ups & Small, Medium Enterprises (SMEs) thru crowd funding companies like Funding Societies, MoolahSense, Capital Match, Co Assets, Minterest & SeedIn. These are Peer – to – Peer Lending schemes that come with their own risks, including complete default of principle invested.

Ending Notes

Just start now. Be it planning, investing or learning anything, the best time to start is now. Utilise compounding (interest) to your advantage.

Leave a comment